Published April 23, 2026

April 2026 Market Report

Thoughts for Sellers

Sellers need to be more competitive in 2026 when listing their homes than at any point over the last several years - but well-priced and well-presented homes continue to move quickly amidst sustainable Buying interest in the Central Oregon lifestyle. With interest rate softening to start the year, Sellers are seeing more Buyers entertain leaving their sweetheart rates from the Covid era. Geopolitical and Macroeconomic headwinds loom, however, and are pushing Sellers to get aggressive in order to get their homes under contract.

Thoughts for Buyers

Buyers can rejoice in increased supply and slight interest rate relief to start the Spring. That said, Prices remain near all-time highs, and Geopolitical and Macroeconomic pressures are keeping many on the sidelines. If buying a home fits your plan - know this: in this market, we are rarely experiencing multiple offer scenarios and most often are seeing Buyers secure quality homes for under the asking price - a scenario which does not exist when interest rates are lower and broader headlines are less uncertain.

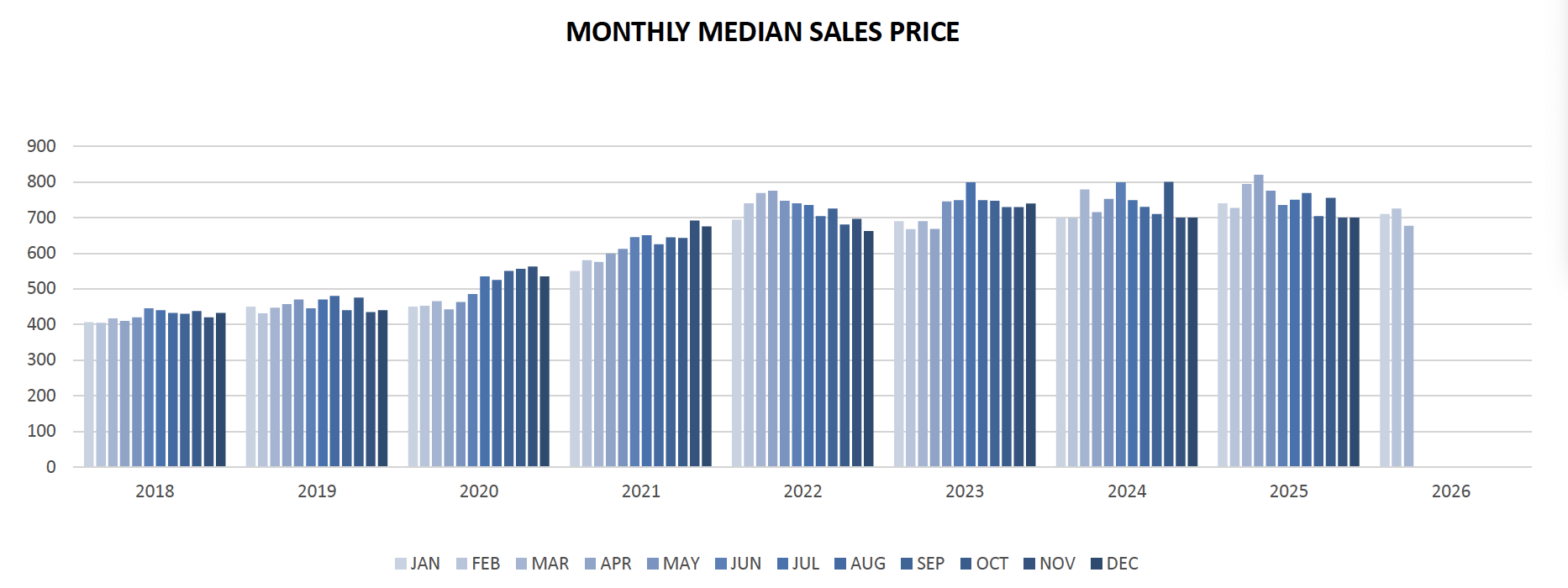

Median Sales Price

Bend’s Median Home Sales Price took a hit in March 2026 -coming in down 15% to March of 2025 @ $677K. While pricing remains below the stronger Spring and Summer peaks of recent years, the Market appears to be holding relatively strong despite concerning March numbers. Well-priced, well-presented homes are still standing out and moving quickly, but broader demand remains sensitive due to affordability, interest rates and macroeconomic uncertainty. Despite current geopolitical issues and negative economic news looming, net migration to the area and sustainable interest in the Central Oregon lifestyle remain strong, and thus, we continue to be impressed by how well the region's Real Estate market is holding up.

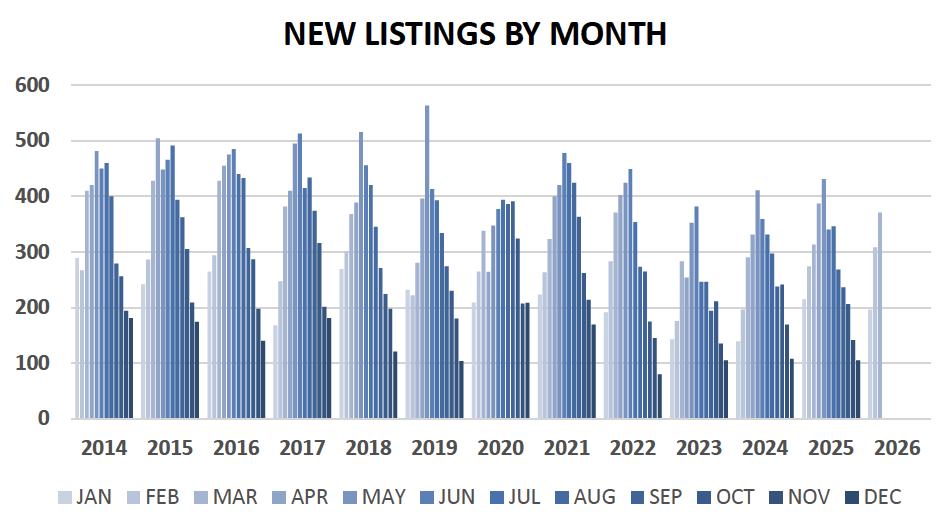

New Listings by Month

New Listings increased notably year-over-year, rising to 371, a 19% increase year-over-year. Activity remains relatively moderate by historical spring standards, but continues to show signs of Inventory build. As more sellers prepare for the seasonal market shift, April & May will be important to watch for a stronger influx of options.

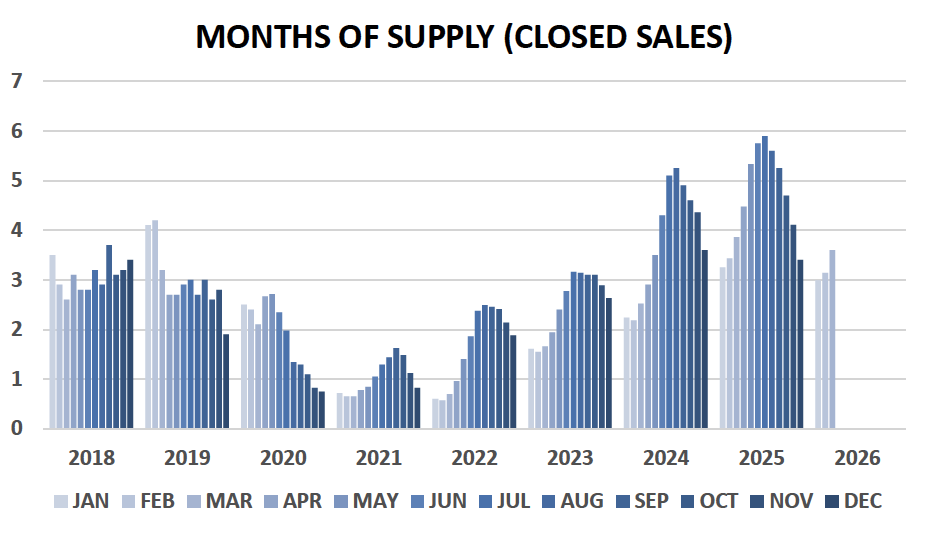

Months of Supply

Months of Supply took a jump to 3.6 months in March, but did remain below March 2025's levels. For now, the market looks more balanced with neither side holding a dramatic advantage, although we do expect to see continued increases in MOS, similar to the trends we've seen since 2022.

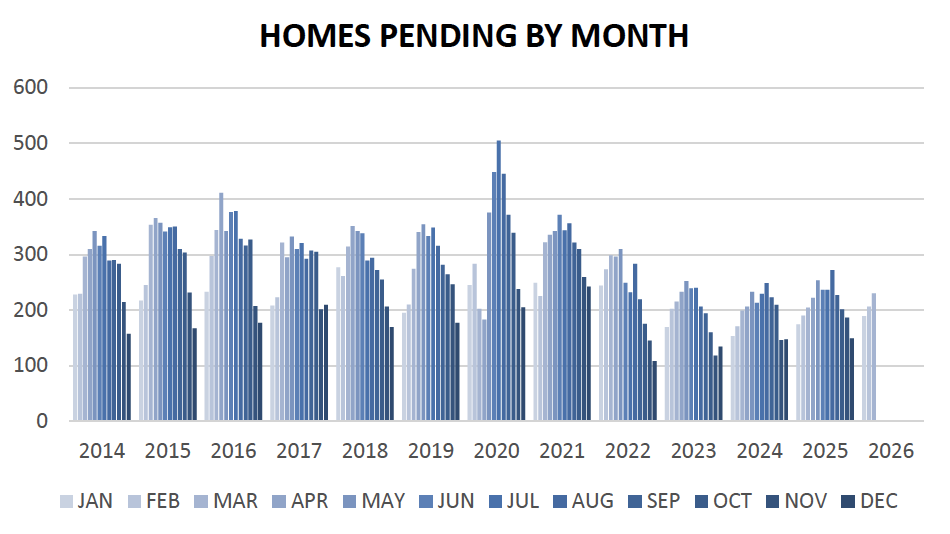

Homes Pending by Month

Pending Home Sales showed a modest increase in March, rising slightly from February and March of 2025 -suggesting early spring buyer activity is beginning to build. The improvement is encouraging, though buyer demand still looks measured rather than aggressive. New listing activity is outpacing pending sales. If this trend continues, expect to see weakness in the market by late Spring and early Summer - similar to what we saw in 2025.

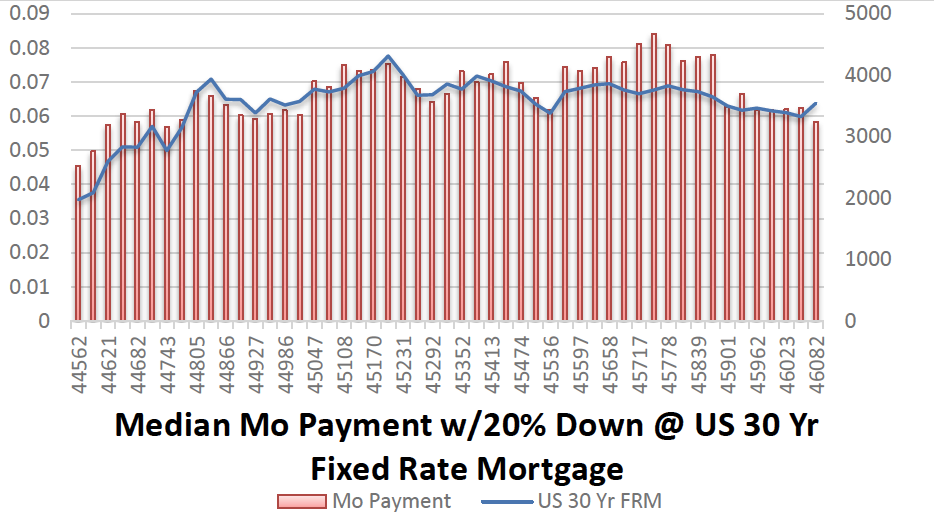

Financing Affordability

The Median Monthly Payment remained near recent lows in March, sitting around the low-to-mid $3,000s per month as mortgage rates hover between 6-6.5%. Compared to the higher payment levels seen through much of 2024 and 2025, affordability has improved modestly, even if it remains a challenge for many buyers. Any further rate relief would likely have an outsized impact on Spring buying demand.

Ryan McGlone

Team Lead - McGlone Property Group | McGlone Property Group | eXp Realty

or another way