The Home Loan Process

Demystifying Home Loans

If you haven’t experienced it before, the home loan process can feel overwhelming, but our team will help you stay informed throughout the process, from pre-approval to closing. The first thing to do is consult with a mortgage specialist (or two). If you don’t already have someone in mind, we partner with some of the best lenders in the industry, and we’d be happy to introduce you, so you’ll be taken care of.

CrossCountry Mortgage

Kevin Peters

About Me

For nearly a decade, Kevin Peters has been providing exceptional financial support to the Bend, Oregon community. A dedicated mortgage loan originator, Kevin works with his customers to ensure a simple and direct path to homeownership. Focused on delivering the best possible loan experience at every turn, Kevin is an expert on a diverse line of loan products, from conventional, FHA, VA and USDA loans to construction, renovation loans and jumbos.

A clear and proactive communicator, Kevin works with his customers to learn their short- and long-term financial goals, enabling him to clearly identify the ideal loan product for their needs. As a steady and patient financial advisor, Kevin ensures that his customers receive the education they need and enthusiastically guides them through the entire loan process.

CrossCountry Mortgage

Michael Burdick

About Me

Meet Michael Burdick, a seasoned Loan Consultant from Bend, Oregon. A Seattle native, Michael began his lending career in WA State. Growing up in the outdoors, he found Bend's natural beauty perfect for his active lifestyle.

A proud father of twins, Michael enjoys Airstream camping, hiking, and skiing at Mt. Bachelor with his family. When he's not working, he's e-biking, paddle boarding, or mountain biking. His first love, however, remains skiing.

With 15 years of experience, Michael is dedicated to exceptional customer service and creative financing solutions. At loanDepot, he ensures smooth closings with competitive pricing and options.

Check out @michaelburdickmortgage on IG for market insights!

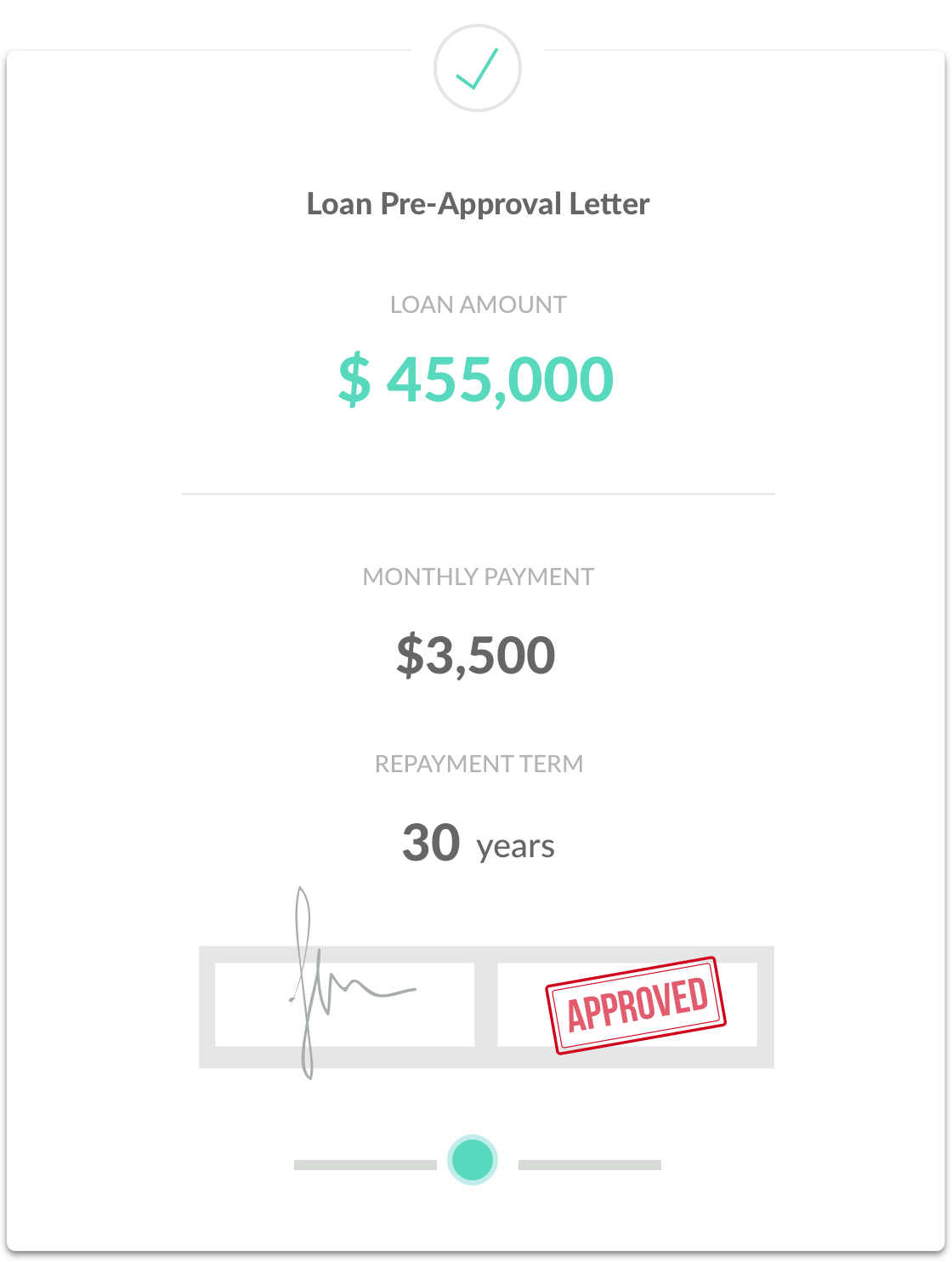

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Loan Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

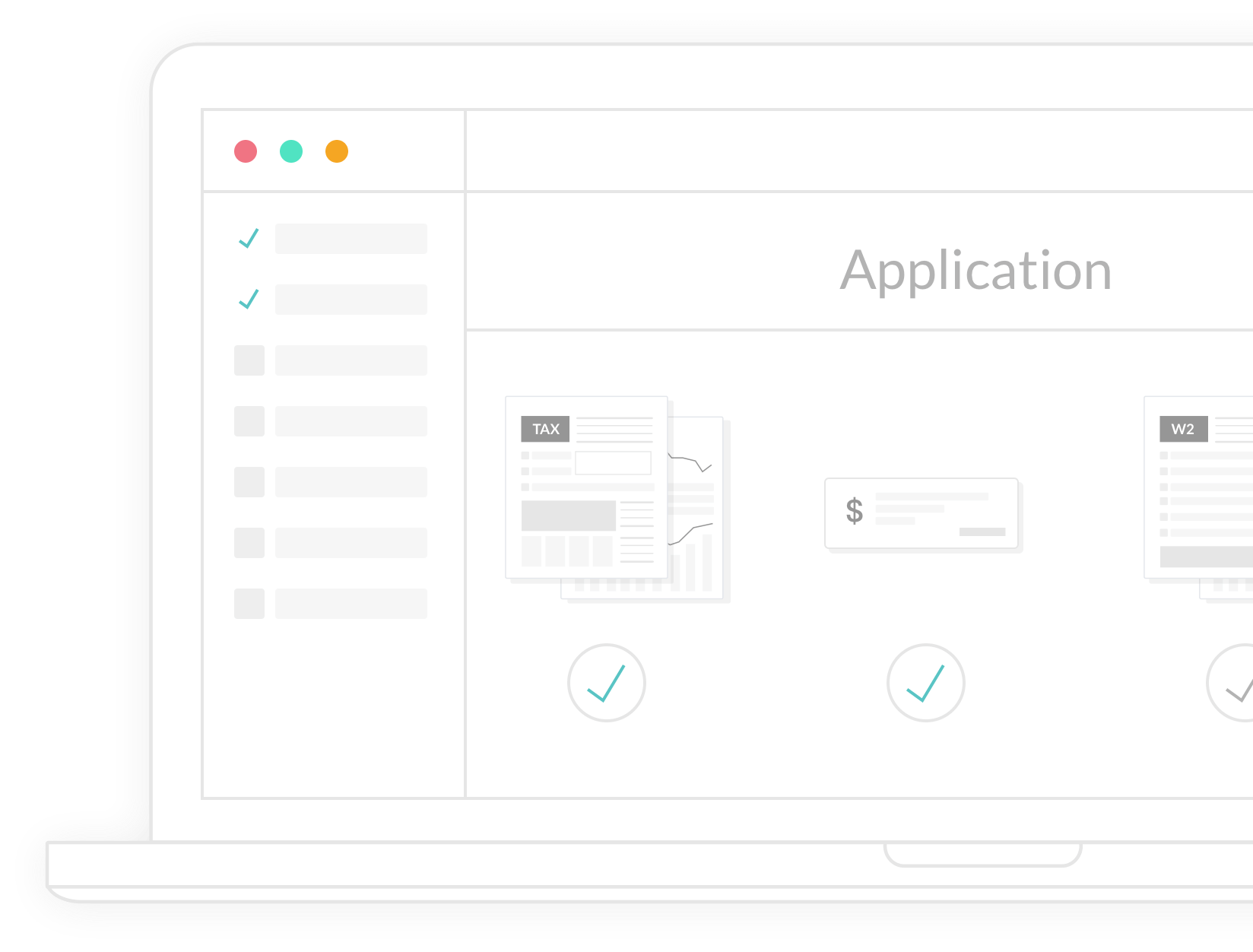

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!