Published July 7, 2025

July 2025 Market Report

Thoughts for Sellers

With Sellers still fetching near "all-time high" prices, it is still a categorically "good time" to sell a home, assuming that you are motivated enough to get a bit more aggressive on price than was necessary a few years ago. With inventory at its highest level in a decade, Sellers need to be more reasonable than in years' past. We do expect unmotivated Sellers to begin pulling their homes from the market come Fall, which will lessen the competition for the truly motivated Sellers.

Thoughts for Buyers

Buyers continue to be challenged by a higher rate environment, but with inventory at its highest level in at least a decade, there are more options for Buyers than ever and motivated Sellers who are willing to take price cuts in order to sell their homes. Get creative with your financing and seek both price reductions and seller credits to help offset interest rates and secure the home you want!

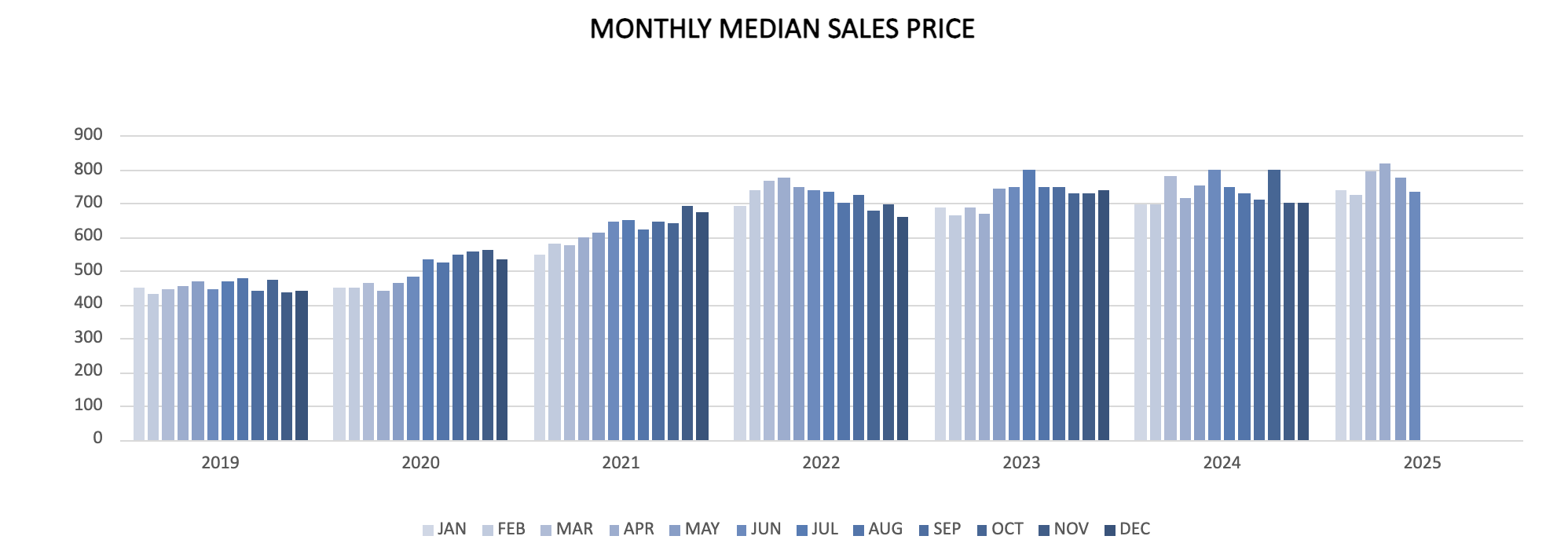

Median Sales Price

Bend’s Median Sales Price dipped -8% Year-Over-Year in June 2025, coming in at $735K. This was also a -5% drop Month-Over-Month from May 2025. We remain in a market that is driven by the less "rate-sensitive" - as the lower price-point market is much slower than the Luxury and higher price-point markets this year. Well-documented this year has been the inventory rise across all price points, which has created headwinds for Sellers. With Months of Supply nearing 6, softening demand may continue to present more favorable conditions for Buyers throughout the Summer. Nationally, we’re seeing a similar trend—especially in markets that experienced sharp price appreciation and increased builder activity over the past four years.

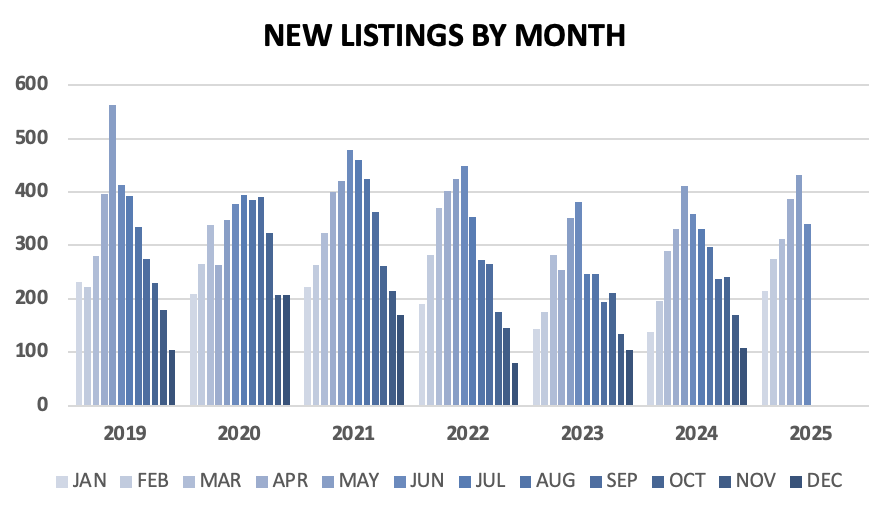

New Listings by Month

New Listings dripped -5% YOY in June 2025, and also dropped -21% MOM to May 2025. Over the prior months, we were seeing a +15% to +20% YOY trend each month. This decline helped keep our Months of Supply below the 6-month level for now. Less motivated Sellers are choosing to sit on the sidelines amidst our inventory rush.

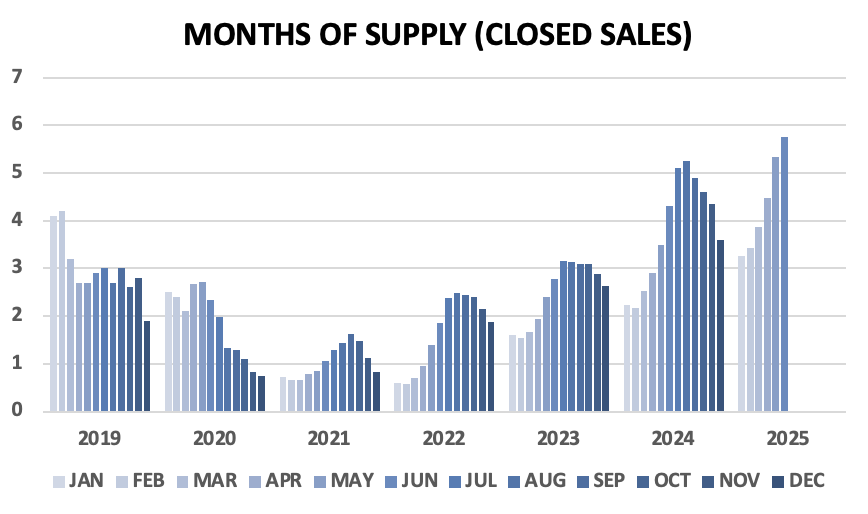

Months of Supply

Months of Supply came in at 5.75 months, representing a 1.5 months of Supply increase (+35%) to June 2024. This jump is mainly due to decreasing buyer activity, as during this same period, we actually saw New Listings soften compared to the trend we've seen over the past several months.

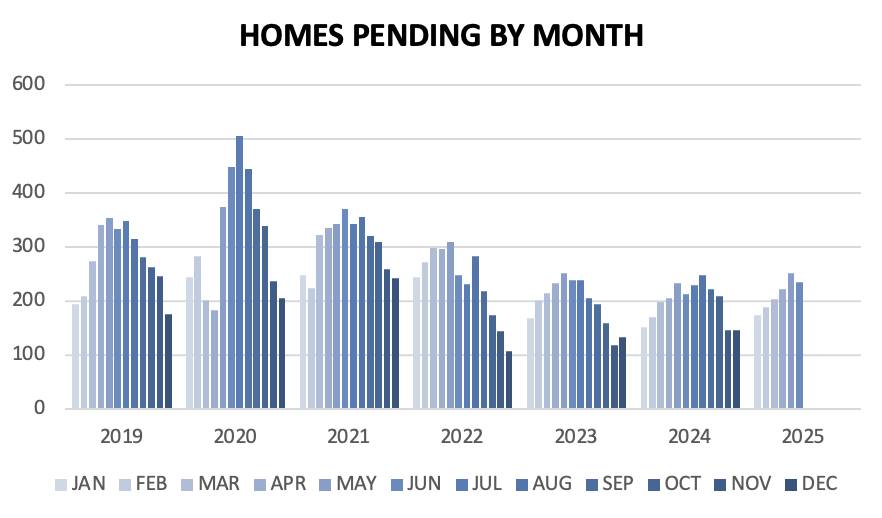

Homes Pending by Month

Pending Units increased YOY for the 11th consecutive month by +11% which is in range of what we've been seeing over the past several months. As inventories continue to build, we do expect to see this number continue to increase, partially due to an increase in availability, and partially due to Sellers taking price reductions.

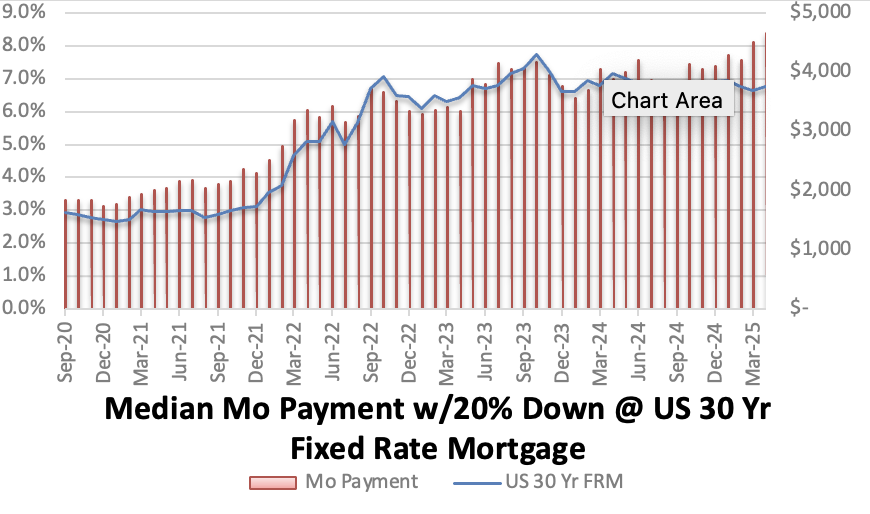

Financing Affordability

The Median Monthly Payment (w/ 20% down @ average FRM) for June 2025 came in at $4,235 - continuing contribution to market stagnation, especially in the <$1M market. We do not expect much meaningful attrition on rates in 2025.