Published September 8, 2025

September 2025 Market Report

Thoughts for Sellers: Sellers can rejoice in some rate relief to start Fall, but they still need to be on-target with pricing and marketing to get their home sold. Despite some reduction in supply in August, we remain at 10-year highs. Inventory is the #1 indicator of market performance. We do expect to see more of our unmotivated Sellers pull their homes from the market as we inch towards the Holidays, which will help reduce options for Buyers

Thoughts for Buyers: Buyers can also rejoice in some rate relief to start Fall, but we remain in a "higher interest rate" environment. With inventory at 10-year highs, Buyers have options and can find "deals" on homes that have sat longer. That said, we are still seeing that Buyers need to move quickly and aggressively on right-priced homes in the most desirable neighborhoods.

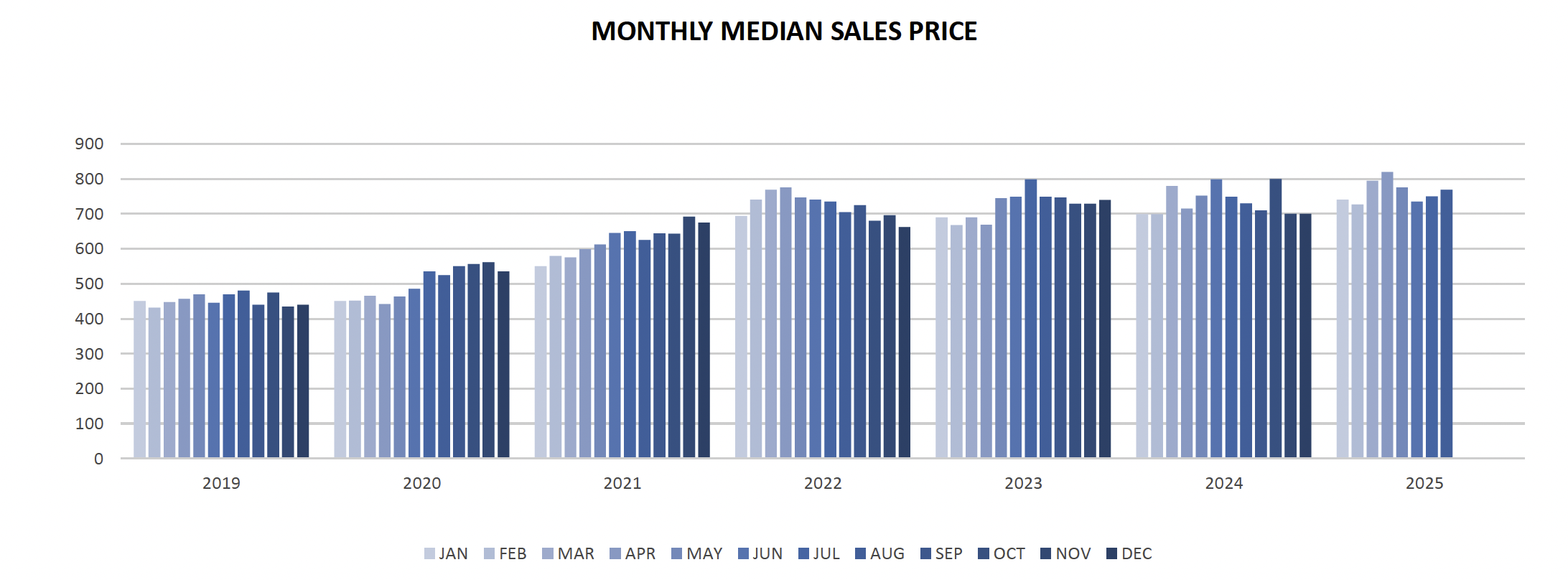

Median Sales Price

Bend’s Median Sales Price was UP +5% Year-Over-Year in August 2025, coming in at $769K, and slightly UP Month-Over-Month from July 2025. We remain in a market that is driven by the less "rate-sensitive" - as the lower price-point market is much slower than the Luxury and higher price-point markets this year. Well-documented this year has been the inventory rise across all price points, which has created headwinds for Sellers. That said, we have started to see inventory decrease as we near Fall - driven by a reduction in New Listings to market, Pending Units hitting a calendar year HIGH in August, and less motivated Sellers starting to pull their homes from the market. Early September is showing signs of interest rate relief as well, which could lead to a Fall market uptick.

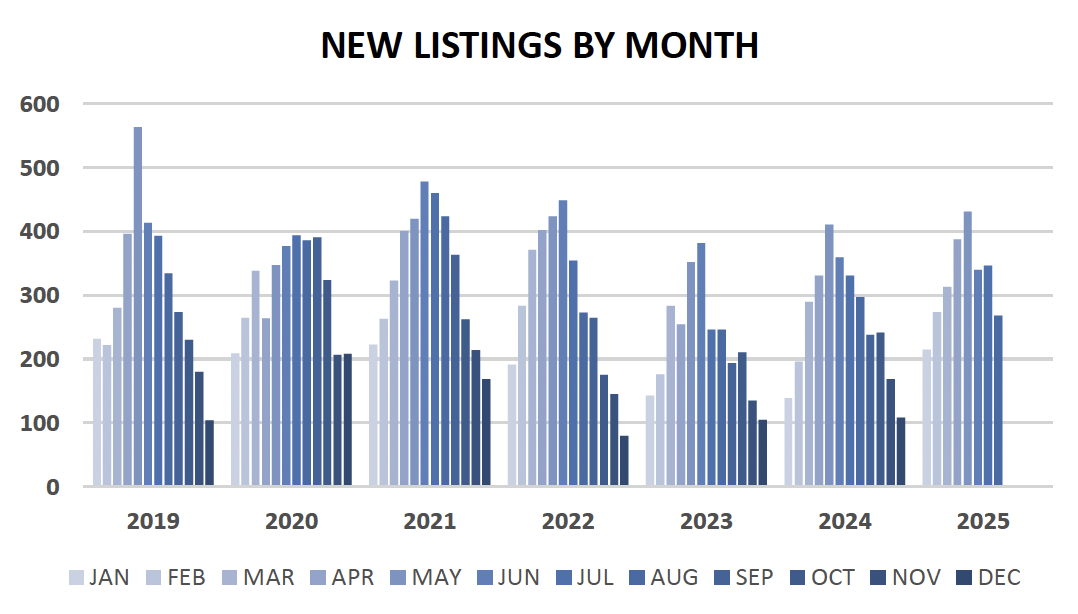

New Listings by Month

New Listings decreased by -10% YOY in August 2025, and also significantly Month-Over-Month to July (-23%), bucking the increased Listing trend which we have seen for most of this year. This decline also helped reduce our Months of Supply from July to August - however, we still remain at 10-year highs in inventory.

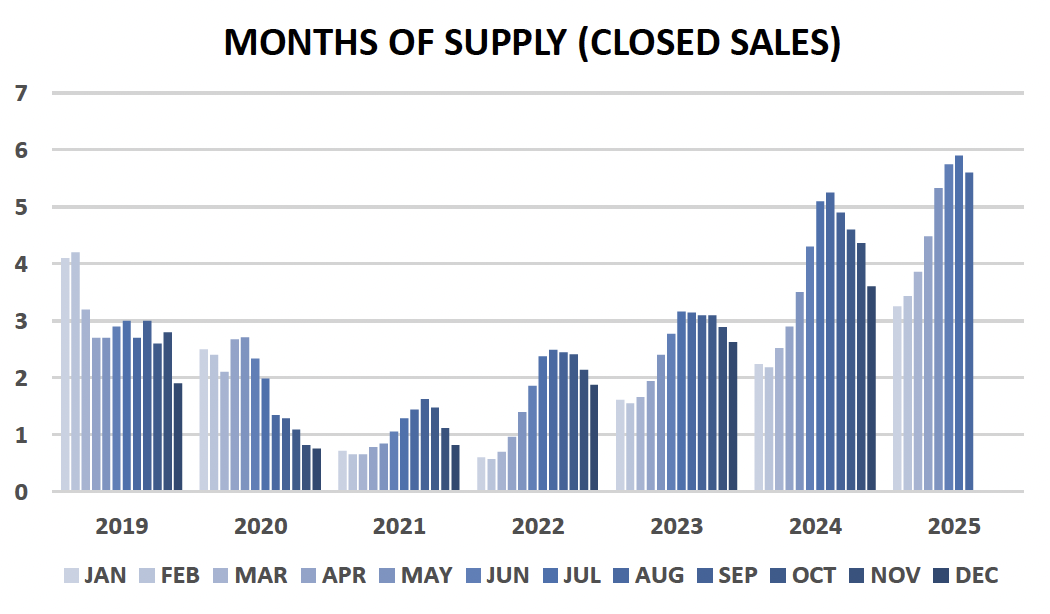

Months of Supply

Months of Supply came in at 5.6 months, representing just a roughly quarter-month increase from August 2024 and the first Month-Over-Month decrease for this calendar year. Albeit, we remain at 10-year highs in supply.

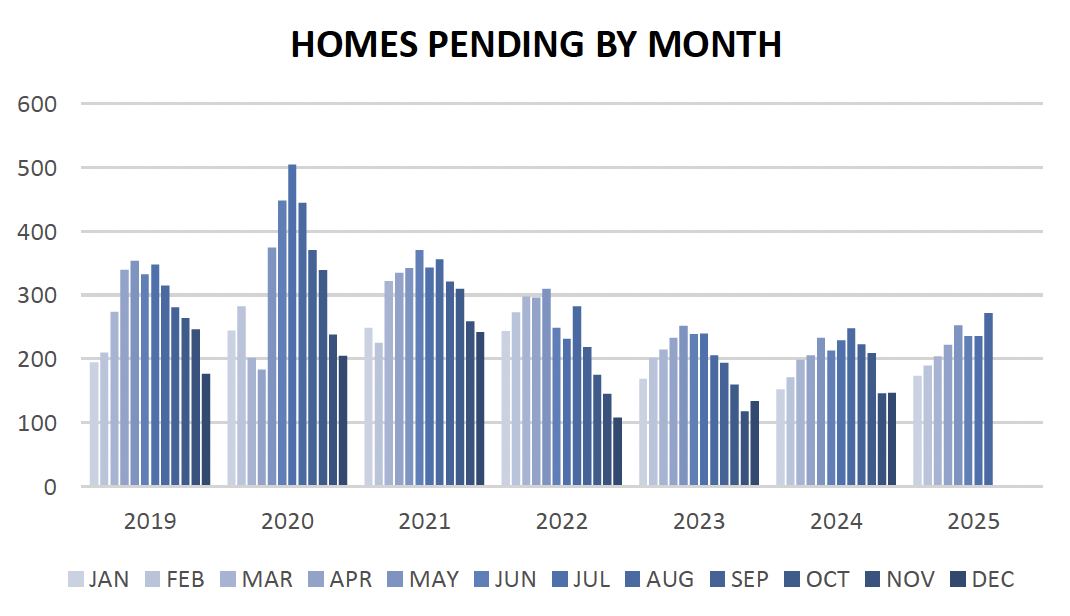

Homes Pending by Month

Pending Units saw an impressive August - posting a calendar year HIGH and a +10% Year-Over-Year increase to August 2024. Likely driven by robust late Summer sales on "stale" inventory, August was also a longer month which saw 5 weekends of open market. All told, this was our 12th consecutive month of increase in Year-Over-Year Pended Units. With signs of rate relief in early September, we may see this trend continue into Fall.

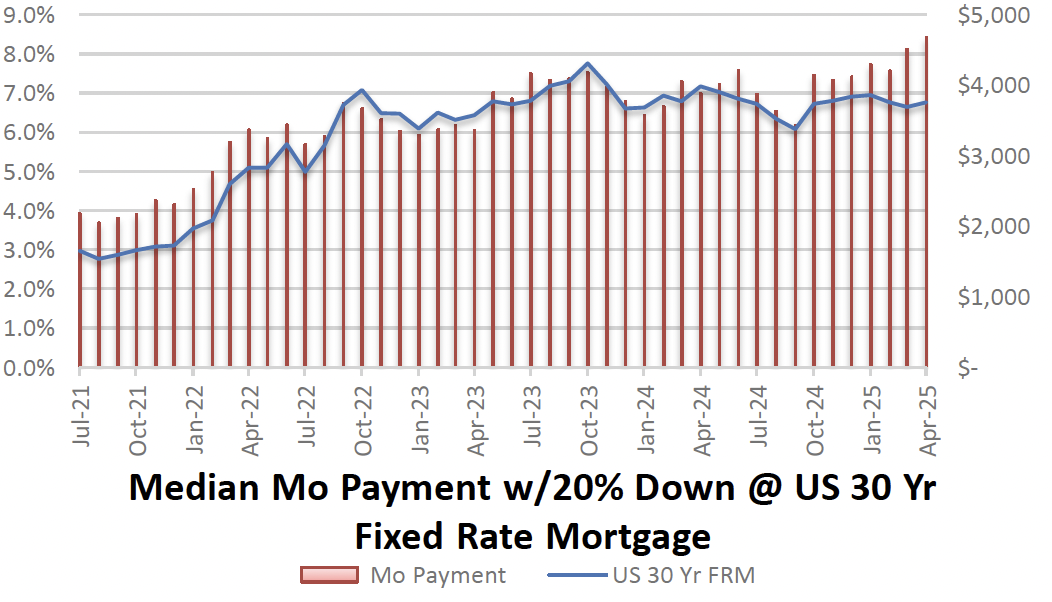

Financing Affordability

The Median Monthly Payment (w/ 20% down @ average FRM) for August 2025 came in at $4,326 - continuing contribution to market stagnation, especially in the <$1M market. Early September is showing signs of rate relief, which we saw last Fall as well - however, we do not anticipate that these reductions will be massive.